Enthusiasts acclaim it as a tremendous opportunity for empowerment while skeptics ask the iconoclastic question “So where’s the problem that’s been lacking for this solution?”. And several commentators have referred to it as a revolution. We’re talking here about blockchains.

Yet what are blockchains, what exactly do they do and what makes the technology so revolutionary?

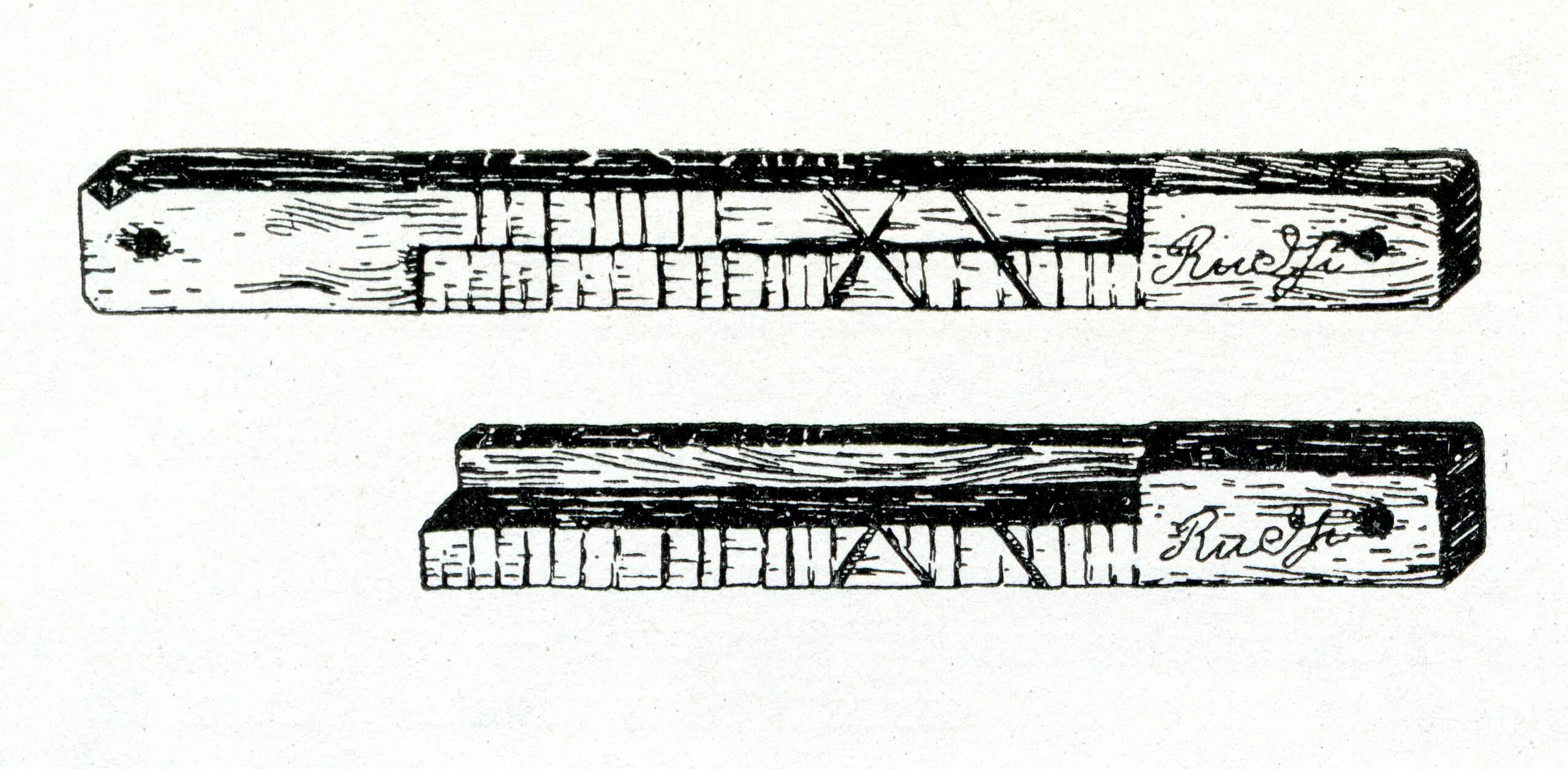

The blockchain concept can hardly be described as new. People have been negotiating trust ever since they started negotiating with one another in the first place. However, such trust is only rarely blind – on the contrary, it is usually protected with the best possible safeguards. “Blockchains” have arguably been around since the Middle Ages, when two or more individuals carved notches in a piece of wood after reaching an agreement. The number of notches indicated the amount of the debt, payments made or goods changing hands. The stick, or “tally”, was then split lengthwise and each party to the transaction received one half – a technique that was deemed to be tamper proof.

Bank as a “middleman”

When two people do business with one another today, a bank is generally involved as an intermediary: the provider receives the payment due to him or her when money flows from one current account to another. In practice, the bank’s role in this transaction is only minor – it simply acts as the “middleman” between two individuals to ensure that there is no breach of trust when the money is handed over.

When two people do business with one another today, a bank is generally involved as an intermediary: the provider receives the payment due to him or her when money flows from one current account to another. In practice, the bank’s role in this transaction is only minor – it simply acts as the “middleman” between two individuals to ensure that there is no breach of trust when the money is handed over.

As far as the business itself is concerned, notaries are totally irrelevant

A notary tends to be called in whenever the objects to be negotiated are more complex. As far as the business itself is concerned, notaries are totally irrelevant; their sole purpose is to record (“notarize”) the legal act. In doing so, they ensure that mutual trust is maintained between all parties.

A blockchain resembles an open book

Blockchains are now set to take on this role. A blockchain resembles an open book – a public ledger based on distributed ledger technology (DLT). The only difference is that it’s digital. It consists of a chain of blocks made up of records. The ledger’s special feature is that every block contains a full copy (“hash”) of the previous block, so that as the number of blocks increases each one not only gets bigger but also more difficult to tamper with. It is impossible to change a past block without changing all of the following blocks. Any attempt to tamper with the blockchain will be immediately noticed – just as it would with a tally – except that in this case, the tally is distributed across umpteen different computers. Instead of a tally stick that is split in order to establish a contract between two people, blockchains store a track on as many entities as possible to prevent tracks (blocks) from being added or deleted. Like the system “bank” or the person “notary”, the construct “blockchain” is designed to build trust.

Trustful relationship

If a block also contains executable code, we use the term “smart contract”. This is a transaction which is automatically executed once the specified conditions are met. For instance, when a house buyer requests an entry in the land register, a sum of money previously deposited with the notary is transferred. A smart contract includes this process from the outset: defined actions are carried out as soon as defined conditions are satisfied. Not even for the logical continuation of the process is an entity necessary.

Reliability of information

The partners collaborating here could be business people. However, devices or systems can just as easily work in this way. Many of the familiar elements in the process industry presuppose reliability of information, in other words a “trustful relationship” between the devices and systems concerned. This raises exciting, fundamental questions for the future. “Is a machine allowed to own a wallet?”, for example. Imagine a driverless car that needs to fill up with gas. Does it then make its way to the fuel dispenser or the charging point and pay using its own money? Digital wallets and distributed payment technologies are logical continuations which have been under discussion for vehicles for some time now.

Blockchains can also be used “as a service”

A number of providers such as Deloitte, SAP or IBM already exist. Blockchains as a service are not at all complicated: a set of data, say from a pharmaceutical manufacturing plant, is sent to the service provider’s blockchain at a defined time. The sender receives a record (block) in return. The blockchain, which grows in size from one transaction to the next, is secured either for life or for a defined time period, so that it is possible to demonstrate at any time that specific values applied at a particular instant during pharmaceutical production.

New technology

Excessive blockchain growth unfortunately remains a structural handicap of the new technology, which is mainly suited at present for low-frequency transactions. If a sensor is queried a hundred times per second, the technology is definitely not yet a viable option. However, if that sensor only supplies one temperature value every ten minutes, it could be validated today using a blockchain without any problem.

Revolution and influence

Blockchain technology undoubtedly has the potential to start a revolution and influence the patterns of daily life. It can take the place of all institutions which only exist because they (purport to) build trust. Notaries and banks, to name but two. A single platform. And absolutely anything to do with currencies. If you hand a hundred dollar bill to someone, that person trusts that slip of paper to be strong and worth the same tomorrow as it is today. And although Germany has experienced several monetary devaluations in the past, we Germans still have considerable trust in our currency.

Founded on trust

All provisions we make for the future or for when we retire are founded on this trust. Cryptocurrencies try to establish a similar degree of trust – and very successfully too – albeit using different mechanisms. The enormous power of traditional “trusters” – the banker’s banks immediately spring to mind here – is beginning to be challenged. It’s a scenario that is bound to appear threatening to those directly affected.

The end of platforms as we know them?

Trust building nowadays frequently takes place on everyone’s favorite platforms – Amazon, Ebay and PayPal are particularly popular. And in the end a bank, too, is nothing more than a platform. Yet if you could buy something direct from a stranger devoid of all risk – and if compliance with contracts of any kind could be automatically verified – then you wouldn’t actually need a platform at all. Public ledgers could mean the end of platforms as we know them. It is this that ultimately what gives the idea its subversive character: the fact that middlemen and gatekeepers will to a large extent be eliminated, from banks through governments to portals. And it is this potential that makes blockchain technology so revolutionary.

Destructive revolutions challenge the status quo

Yet blockchains are likely to feel a strong headwind, especially – though not only – from financial regulators. And the technology itself is (still) dogged by problems on several different fronts.

There are destructive revolutions that challenge the status quo. And there are productive revolutions that explore new paths and render the status quo superfluous. What do you think? How will blockchains change the world we live in?

For the first time as a video: New column by Dr. Andreas Helget is online